SEC’s Mandatory Climate Disclosures

The SEC just passed a major climate disclosure rule. Find out what it means for emissions reporting and your company’s compliance.

.png)

This morning, the U.S. Securities and Exchange Commission (SEC) voted to adopt a long-awaited climate disclosure rule. SEC Chair Gary Gensler, Commissioner Caroline Crenshaw and Commissioner Jaime Lizárraga voted in favor of the rules at an open commission meeting, almost two years after the agency released its initial proposal.

The Securities and Exchange Commission rules aim to standardize climate-related company disclosures about greenhouse gas emissions, risks, and how much money they are spending on the transition to a low-carbon economy. This disclosure is important for investors, suppliers, customers to decide which companies to partner with or purchase from.

Although the new rules omit Scope 3 from mandated disclosures, the passage of the SEC Climate Rules, requiring companies to disclose Scopes 1 and 2 are critical and get the United States closer to competing globally with sustainability leaders in Europe and the U.K., and fulfill the country’s commitment to the Paris Agreement.

<span class="small-blockquote">"A lot has changed in the last 14 years since that 2010 climate guidance. Far more investors are making investment decisions that are informed by climate risk, and far more companies are making disclosures about climate risk.”</span>

<span class="blockquote-wrap">

<strong>Gary Gensler</strong>

SEC Chair

</span>

What Companies are Required to Disclose

Though we recommend every company has a deep understanding of its emissions and climate-related risks, not every U.S. company is required to report to the SEC, just companies that are publicly traded in the U.S. So, if you can buy their stock on an exchange like the New York Stock Exchange or Nasdaq, they've got to start getting more transparent about their climate impact.

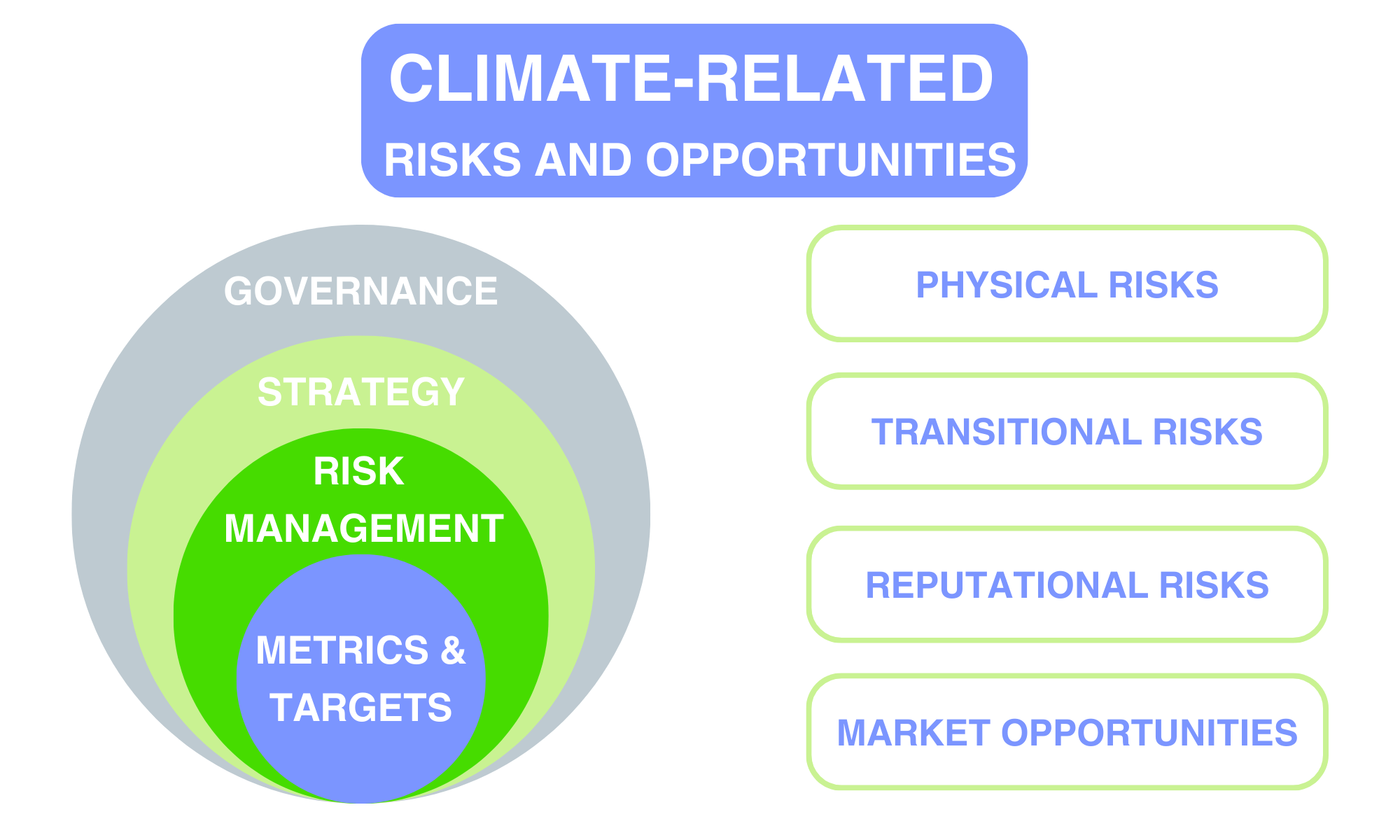

Alignment with Taskforce on Climate-related Financial Disclosures (TCFD)

The TCFD is the North Star for climate reporting and the SEC’s rules are steering companies in its direction. The TCFD framework encourages companies to disclose climate-related risks and opportunities, and the SEC’s rules echo this by emphasizing transparency and accountability in financial reporting.

The Rule Elements: A Deeper Dive

1. Narrative Disclosures: This is where companies tell their climate story. They'll talk about the climate risks they face, how they deal with them, and their sustainability goals. It's all about giving investors and customers a clear picture of their climate practices. Narrative Disclosures align with the recommendations and framework of the Taskforce on Climate-related Financial Disclosures, which has been adopted globally.

The TCFD framework recommends that companies disclose information in four key areas: Governance, Strategy, Risk Management, and Metrics & Targets. Here's how these areas relate to the Narrative Disclosures under the SEC's new rules:

- Governance: This is all about who's calling the shots on climate issues within the company. Companies should share how their board and management are overseeing climate-related risks and opportunities.

- Strategy: Here, companies need to disclose how climate change might affect their business in the short, medium, and long term. They should talk about things like how rising sea levels could impact their coastal facilities or how a shift to renewable energy might open up new markets. It's about painting a picture of their game plan in a warming world.

- Risk Management: This is where companies get down to the nitty-gritty of how they're dealing with climate risks. They should describe the processes they have in place to identify, assess, and manage these risks. It's like showing investors their toolkit for fixing leaks and patching holes in their climate defense strategy.

- Metrics & Targets: Finally, companies should share the metrics they use to measure their climate impact and the targets they've set to reduce it. They need to include things like their greenhouse gas emissions, energy usage, and progress towards sustainability goals. It's like giving investors a scoreboard to track the company's climate performance.

2. Independent Attestation: This is the trust factor. Companies can't just say they're doing great things for the climate; they need someone else to back up their claims. An independent third party, like Planet FWD, checks the company's greenhouse gas emissions data to make sure it's accurate. Think of this as a referee in a game, ensuring everyone plays by the rules.

3. Financial Statements: This is where the rubber meets the road. Companies have to show how climate issues are affecting their money matters. For example, if a food company's farms are in a flood-prone area, they need to tell investors how this risk could hit their wallet. It's all about connecting the dots between climate change and financial health.

What Emission Scopes are Included

As reported by Forbes, “the current U.S. materiality standard comes from a 1976 Supreme Court decision TSC Industries, Inc. v. Northway Inc., in which the Court stated “a substantial likelihood that a reasonable shareholder would consider it important in deciding how to vote…Put another way, there must be a substantial likelihood that the disclosure of the omitted fact would have been viewed by the reasonable investor as having significantly altered the ‘total mix’ of information made available.’”

Scope 1 Material Risks:

Also known as “direct emissions from greenhouse gases (GHG).” Companies report GHG emissions from sources they own or control as scope 1. Direct GHG emissions are principally the result of the following types of activities undertaken by the company: generation of electricity, heat, or steam; physical or chemical processing; transportation of materials, products, waste, and employees; and fugitive emissions.

Scope 2 Material Risks: Also known as “electricity indirect emissions from greenhouse gases (GHG),” Scope 2 includes company emissions from the generation of purchased electricity that is consumed in its equipment or operations.

What’s Not Included

Scope 3 Material Risks: Also known as “other indirect emissions from greenhouse gases (GHG).” Scope 3 provides an opportunity for brands to be innovative in GHG management. Activities considered Scope 3 include the following: extraction and production of purchased materials and fuels; transport-related activities; electricity-related activities not included in Scope 2 (e.g. extraction, production, and transportation of fuels consumed in the generation of electricity; purchase of electricity that is sold to an end user, reported by the utility company; generation of electricity that is consumed in a T&D system, reported by end-user; leased assets, franchises, and outsourced activities; use of sold products and services; waste disposal activities.)

Why Scope 3 matters: For most companies, but especially for a CPG, food, or grocery company, Scope 3 emissions make up the majority of emissions (90%+ avg.).

Large companies doing business in California or Europe need to comply with the European Union’s Corporate Sustainability Reporting Directive and California’s disclosure laws. It would make sense that the SEC law would align for reporting purposes. The absence of Scope 3 and double materiality requirements in the SEC law could cause extra complexity in reporting compliance for these companies. The CSRD’s Scope 3 reporting requirements, which mandate that companies take a double materiality approach, are far more extensive, and similarly, California’s SB 253 also mandates Scope 3 reporting.

That said, beverage, food, and consumer goods companies that are true leaders and innovators in climate action will be measuring and reporting Scope 3, regardless of requirements by the SEC. And just because Scope 3 has been omitted in this ruling does not mean it will never be included.

<span class="small-blockquote">"In the proposal, we took a layered approach to disclosure of Scope 3 greenhouse gas emissions. While many investors today are using Scope 3 information in their investment decision-making, based upon public feedback, we are not requiring Scope 3 emissions disclosure at this time."</span>

<span class="blockquote-wrap">

<strong>Gary Gensler</strong>

SEC Chair

</span>

Future Legal Concerns

Legal challenges to the new ruling are likely and widely reported. Concerns over whether the rules could withstand a legal challenge are fueled by a 2022 Supreme Court decision, which curbed the Environmental Protection Agency's power to regulate emissions. The legal challenges we are already seeing for California Climate Bills, which passed in October 2024, are also a warning sign that this new SEC ruling will garner legal scrutiny.

Timing and Phase-In Period

The largest companies must start making some climate disclosures as early as fiscal 2025 and about greenhouse gas emissions as soon as fiscal 2026. Given how extensive this ruling is, we recommend affected companies begin preparing for disclosures as soon as possible (as reported by CNBC).

We are here to help

Planet FWD firmly stands behind the SEC climate rules and we agree that investors, consumers, and other stakeholders deserve transparency from companies, particularly consumer goods companies, regarding their greenhouse gas (GHG) emissions to inform decision-making. The signing of these laws is a huge step in the right direction for climate transparency and decarbonization. We also acknowledge that widespread adoption will be challenging and will require close partnerships and collaboration across the supply chain.

Planet FWD is uniquely positioned to partner with global food and CPG companies, retailers, and their suppliers to meet the U.S. SEC requirements. Planet FWD helps companies calculate and report their greenhouse gas emissions across Scopes 1, 2, and 3. We uncover the drivers of their supply chain emissions using our lifecycle database of thousands of ingredients and materials and work with suppliers to reduce their Scope 3 emissions. In addition, Planet FWD is positioned to enable third-party verification of results to meet the requirements of this climate legislation. In collaboration, we can get ahead of climate regulation and ensure the industry has the insights it needs to satisfy all disclosure requirements.

Head of marketing

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Consectetur, adipiscing elit, sed do eiusmod tempor incididunt ut lab. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Lorem ipsum dolor sit amet, consectetur adipiscing elit.

This is an example blog post style

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Sed vulputate odio ut enim. Volutpat sed cras ornare arcu dui. Lorem dolor sed viverra ipsum. Luctus accumsan tortor posuere ac ut consequat semper. Viverra justo nec ultrices dui sapien eget mi proin. Mollis nunc sed id semper risus in hendrerit gravida rutrum. Lacinia quis vel eros donec. Nisi vitae suscipit tellus mauris a diam. Ac orci phasellus egestas tellus rutrum tellus pellentesque eu tincidunt. Morbi quis commodo odio aenean sed adipiscing diam. Urna duis convallis convallis tellus id interdum. Tortor vitae purus faucibus ornare suspendisse sed. Vehicula ipsum a arcu cursus vitae congue. Enim sed faucibus turpis in. Orci eu lobortis elementum nibh tellus molestie nunc non blandit.

Nunc id cursus metus aliquam eleifend mi in. A erat nam at lectus urna duis convallis convallis. Tristique senectus et netus et malesuada fames ac. Id interdum velit laoreet id donec. Egestas dui id ornare arcu odio. Gravida rutrum quisque non tellus orci ac auctor. Malesuada fames ac turpis egestas maecenas pharetra convallis. Ut diam quam nulla porttitor. Eget nunc lobortis mattis aliquam faucibus purus. Aenean sed adipiscing diam donec adipiscing tristique risus nec. Nisi est sit amet facilisis magna etiam tempor orci eu. Tortor posuere ac ut consequat.

“Lorem ipsum dolor sit amet, consectetur adipiscing elit”

<span class="blockquote-wrap">

<strong>Naomi</strong>

Head of marketing

</span>

This is an example blog post style

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Sed vulputate odio ut enim. Volutpat sed cras ornare arcu dui. Lorem dolor sed viverra ipsum. Luctus accumsan tortor posuere ac ut consequat semper. Viverra justo nec ultrices dui sapien eget mi proin. Mollis nunc sed id semper risus in hendrerit gravida rutrum. Lacinia quis vel eros donec. Nisi vitae suscipit tellus mauris a diam. Ac orci phasellus egestas tellus rutrum tellus pellentesque eu tincidunt. Morbi quis commodo odio aenean sed adipiscing diam. Urna duis convallis convallis tellus id interdum. Tortor vitae purus faucibus ornare suspendisse sed. Vehicula ipsum a arcu cursus vitae congue. Enim sed faucibus turpis in. Orci eu lobortis elementum nibh tellus molestie nunc non blandit.

<span class="rtb-protip">

<span class="rtb-protip-title"></span>

<span class="rtb-protip-body">Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim.</span></span>

How to customize formatting for each rich text

- Lorem ipsum dolor sit amet, consectetur adipiscing elit sed do eiusmod

- Lorem ipsum dolor sit amet, consectetur adipiscing elit sed do eiusmod

- Lorem ipsum dolor sit amet, consectetur adipiscing elit sed do eiusmod

- Lorem ipsum dolor sit amet, consectetur adipiscing elit sed do eiusmod

Headings, paragraphs, blockquotes, figures, images, and figure captions can all be styled after a class is added to the rich text element using the "When inside of" nested selector system.

Static and dynamic content editing

A rich text element can be used with static or dynamic content. For static content, just drop it into any page and begin editing. For dynamic content, add a rich text field to any collection and then connect a rich text element to that field in the settings panel. Voila!

- Lorem ipsum dolor sit amet, consectetur adipiscing elit sed do eiusmod

- For static content, just drop it into any page and begin editing. For static content, just drop it into any page and begin editing.

- Lorem ipsum dolor sit amet, consectetur adipiscing

How to customize formatting for each heading

Headings, paragraphs, blockquotes, figures, images, and figure captions can all be styled after a class is added to the rich text element using the "When inside of" nested selector system.